7 Common Misconceptions About Buying a House

Whether buying a house is a future goal or you’re already actively shopping your local housing market, home buying is a ...

Read More

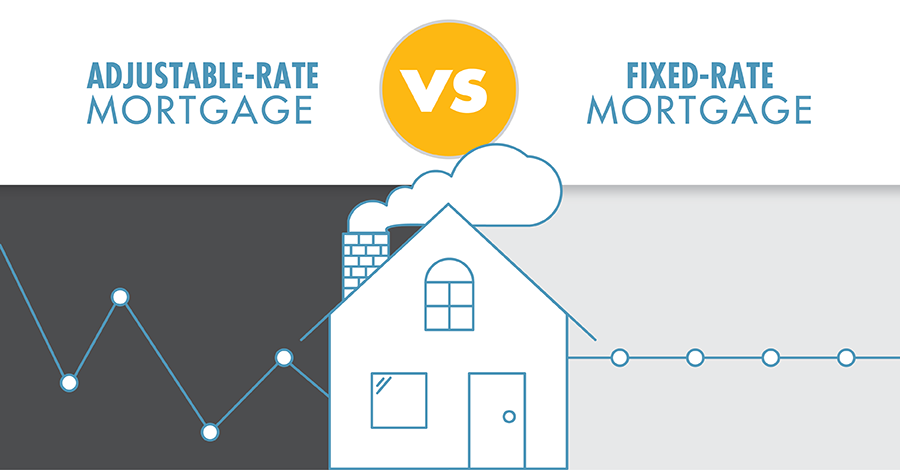

Consolidated Community Credit Union is here to guide you through the differences between an adjustable-rate mortgage (ARM) and a fixed-rate mortgage so you can make the best decision when it comes to Portland home buying.

Whether you’re a first-time home buyer or are already in the Portland housing market, navigating your residential real estate options can be a complicated and confusing process. Not only do you need to choose a trusted lender, but you also have to figure out which type of mortgage is right for you.

While there are several types of mortgages offered by credit unions and banks, most people opt for a fixed-rate mortgage when buying a home. However, that doesn’t necessarily mean it’s the right choice for you. An adjustable-rate mortgage may come with a lower initial interest rate or a repayment term that’s more suitable for your needs. Keep reading to learn about different home financing options to learn how to decide which mortgage loan is best for you.

First things first: What’s an adjustable-rate mortgage? And what’s a fixed-rate mortgage? For all mortgages, the interest rate will be applied to the outstanding balance of your loan, but depending on the type of loan you choose, how it accrues may or may not remain constant. This means you need to consider how your income will either grow or stay the same.

With an adjustable-rate mortgage (ARM), your interest rate will vary throughout the life of your loan. After an initial period, the rate will reset periodically at preset benchmarks, either annually or sometimes monthly. The newly adjusted rate, referred to as an ARM margin, is based on the index plus an additional spread.

Conversely, with a fixed-rate mortgage, you will keep the same interest rate throughout the entire life of your loan. This means that your total monthly payment, including principal and interest, will remain the same unless your property taxes or homeowner’s insurance changes. Knowing how much your mortgage payments will be can be both comforting and useful for homeowners. It makes budgeting easier, and if your income goes up throughout the years, your adjusted cost of living will decrease with steady monthly payments.

Fixed-rate loans are one of the more popular types of mortgages for qualifying buyers in Oregon or Washington, but it’s not a one-size-fits-all option. Fixed-rate mortgages typically have higher starting interest rates than ARMs, which may impact the home you can afford.

Adjustable-rate mortgage: An adjustable-rate mortgage offers lower initial interest rates. This means that lenders can take a lower payment into account when they qualify you for a loan, which may allow you to afford a more expensive home than you would with a fixed-rate mortgage. Another benefit of an ARM is that homeowners don’t need to refinance when interest rates fall –– instead, they can sit back and watch their monthly payments adjust with the market. An ARM can be cost-effective for those who don’t plan to live in a home for very long or those who predict their income to increase over time.

Fixed-rate mortgage: Fixed-rate loan tends to be beneficial for people who intend to stay where they are for several years or even decades. The main advantage of a fixed-rate loan is that the borrower is protected from sudden increases if interest rates rise. And though the interest rate is fixed, how much interest you pay will change depending on how long the loan term is. However, you can always refinance to more favorable terms if your interest rate drops.

When choosing a mortgage, you need to consider a wide range of personal and financial factors. It’s also important to consider economic realities that are always changing. But in general, it’s important to ask yourself four questions when choosing your home loan type.

When selecting your home loan, it is also helpful to run a few initial calculations to determine the worst-case scenario. Calculating your mortgage at various interest rates can help you plan long-term if a fixed-rate or adjustable-rate mortgage will be better for your situation.

Now that you’re familiar with the difference between a fixed-rate and an ARM loan, you’ll be able to make an informed decision about which type of home loan to choose. If there’s a good chance that your income will increase in the next decade or if you plan to move within a few years, an adjustable-rate mortgage could be the right choice.

Buying a home is a major life milestone, and it comes with several crucial decisions that shouldn’t be taken lightly. Be sure to weigh your options, and don’t be afraid to ask your lender lots of questions before committing to anything. Check out the mortgage tools and loan programs from Consolidated Community Credit Union, and speak to a local lender to get a mortgage in Portland and Hood River that works for your unique needs and budget. If you’re ready to get started on the home-buying process, apply for a mortgage today!

.png?width=3509&height=6976&name=4%20questions%20to%20ask%20yourself%20to%20know%20which%20home%20loan%20is%20right%20for%20you!-01(1).png)