Credit Cards: Friend or Foe to Your Finances?

Blog Highlights Benefits: Learn how to use credit cards as a financial tool to build credit, earn rewards, and enjoy ...

Read More

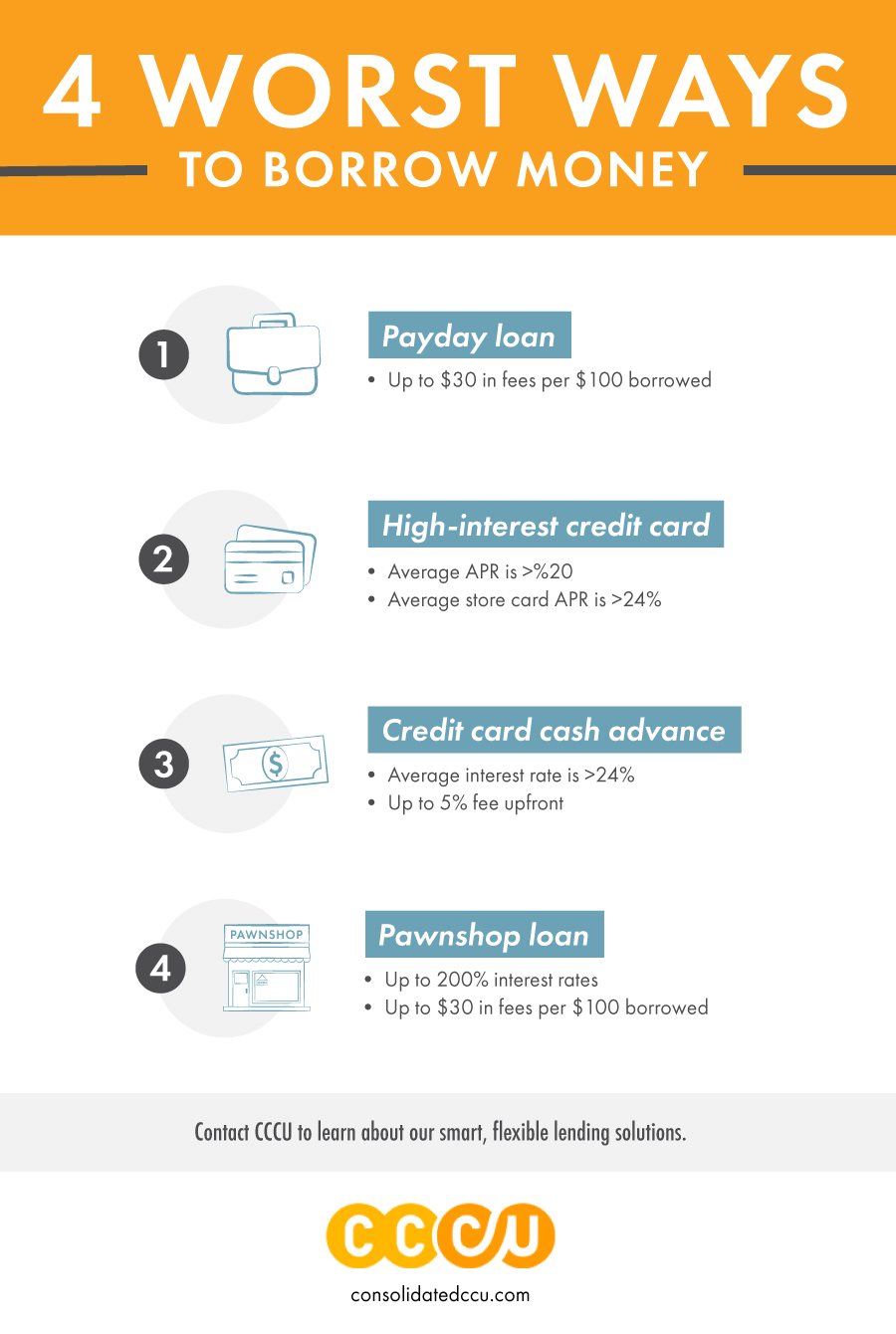

Borrowing money is often a fact of life. Whether it's to enter the real estate market, attend school, or launch a business, it can ultimately be a financially sound choice and potentially pay off in the long run if managed correctly.

But not all funding methods are better than others. So, why are some options riskier, and which should you avoid? Read on to find out!